Your teen just had their first accident and you're facing a premium increase that could push $4,000–$6,000 annually. Adding a teen driver already doubles most premiums in Michigan — add an at-fault accident and the surcharge compounds, but specific carriers and discount strategies can cut that increase by 30–40%.

How Much Does Adding a Teen With One Accident Cost in Michigan?

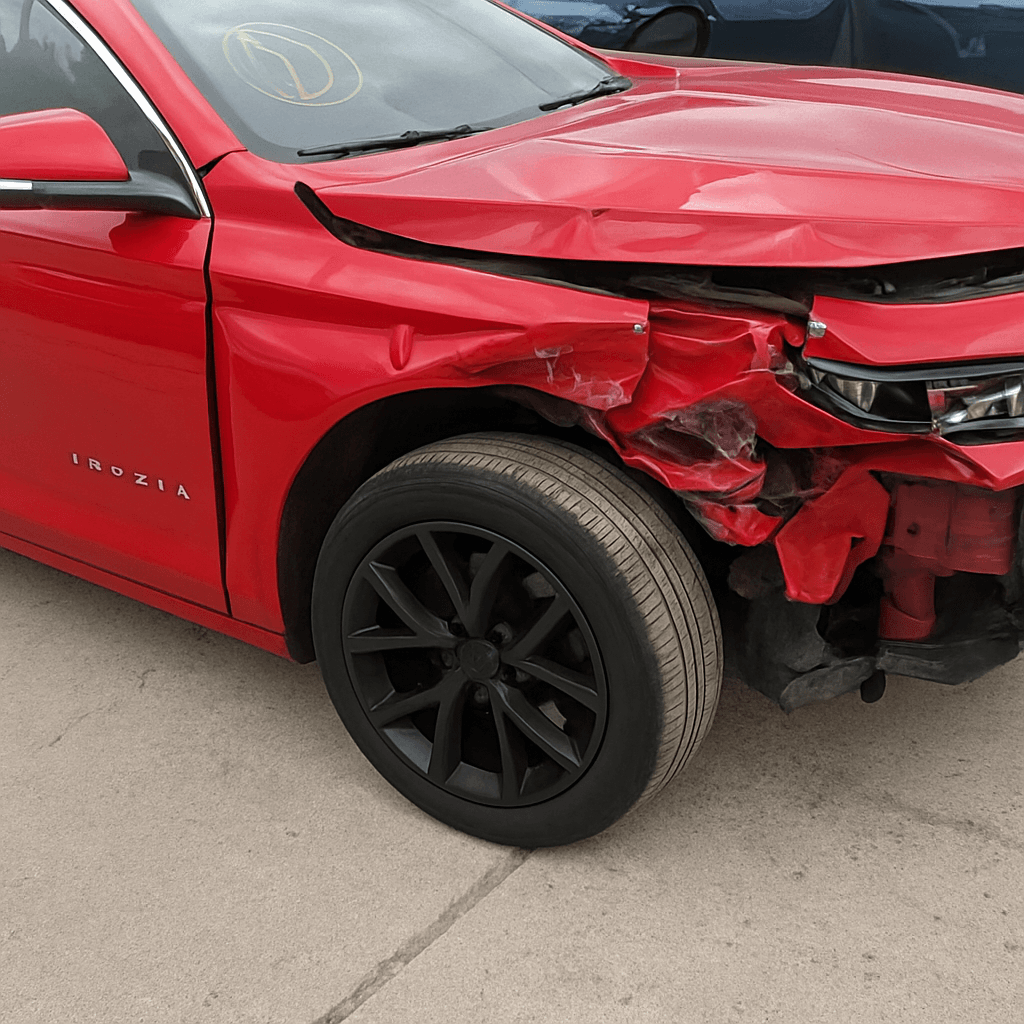

Adding a 16-year-old driver to a Michigan auto policy typically increases the annual premium by $2,800–$4,200 depending on the vehicle and coverage level. An at-fault accident adds another 40–60% surcharge on top of the teen driver rate increase, pushing total combined increases to $4,500–$6,500 annually for the first policy term after both the addition and the accident.

Michigan's no-fault system and unlimited PIP requirements make base premiums higher than most states, which means percentage increases from teen drivers and accidents translate to larger dollar amounts. A parent paying $2,400/year for full coverage on two vehicles might see that jump to $7,000–$8,500 after adding a teen with one accident.

The surcharge duration matters. Most Michigan carriers apply accident surcharges for three years from the incident date. The teen driver surcharge gradually decreases as the driver ages and gains experience, typically dropping 15–25% at age 18, another 20–30% at age 21, and reaching standard adult rates by age 25 if no additional violations occur.

Which Carriers in Michigan Offer the Best Rates for Teen Drivers With Accidents?

State Farm, Auto-Owners, and Progressive consistently rank among the most competitive carriers for Michigan families adding teen drivers with accidents, but which one offers the lowest rate depends on the parent's existing driving record, the vehicle the teen will drive, and whether the teen qualifies for good student or telematics discounts.

State Farm's discount stacking structure allows parents to layer the good student discount (typically 15–25%), Steer Clear driver training discount (up to 15%), and Drive Safe & Save telematics program (5–30% based on driving behavior) on the same policy. For a teen with one accident, enrolling in Drive Safe & Save before the policy renews can demonstrate improved driving behavior and reduce the accident surcharge by 20–35% after six months of clean telematics data.

Auto-Owners tends to offer lower base premiums for families in suburban and rural Michigan counties, and their accident forgiveness program (available to policyholders with five years claim-free history) can waive the first accident surcharge entirely if the parent has the coverage in place before the teen's accident occurs. Progressive's Snapshot program offers immediate rate reductions for safe driving behavior, which can offset teen and accident surcharges within the first policy term if the teen demonstrates consistent safe habits.

Avoid carriers that do not offer telematics programs or good student discounts in Michigan. The inability to demonstrate improved driving behavior post-accident or academic responsibility leaves you paying the full surcharge for the entire three-year period.

See what adding a teen driver actually costs in your state

Compare quotes from carriers that offer good student discounts — most parents find savings they didn't know were available.

Get Your Free Quote✓ Good Student Discounts✓ No Obligation✓ Licensed Carriers✓ All 50 States

Should You Add Your Teen to Your Policy or Get Them a Separate Policy After an Accident?

Add your teen to your existing policy in nearly every scenario. A standalone teen policy with one accident will cost $8,000–$14,000 annually in Michigan due to unlimited PIP requirements, lack of multi-vehicle and homeowner bundling discounts, and the compounded young driver and accident surcharges applied without a mature driver's history to offset them.

The only time a separate policy makes financial sense is if the parent's driving record includes multiple violations or accidents themselves, creating a situation where the parent's surcharges compound the teen's. In that scenario, placing the teen on a grandparent's or other family member's policy (if they consent and live in the same household or the teen is listed as a regular driver of that household's vehicle) can reduce total household insurance costs.

When you add your teen to your policy, make sure to assign them to the least expensive vehicle in your household if you own multiple cars. Michigan allows named driver exclusions, but excluding your teen from specific vehicles requires written documentation and does not reduce the base teen surcharge — you're simply limiting which cars they can legally drive under your coverage.

What Discounts Can Reduce the Premium for a Teen Driver With an Accident?

The good student discount is the highest-value tool available. Michigan does not mandate this discount, but most carriers offer 10–25% reductions for students maintaining a B average or 3.0 GPA. Proof is required at policy inception and typically every six or twelve months — parents who don't submit updated transcripts lose the discount mid-policy without notification.

Telematics programs like State Farm's Drive Safe & Save, Progressive's Snapshot, or Allstate's Drivewise monitor acceleration, braking, speed, and mileage. For a teen driver with one accident, enrolling immediately after the incident allows them to demonstrate improved driving behavior and reduce the accident surcharge by 20–40% after six months of safe driving data. Most programs offer a small participation discount (5–10%) at enrollment, with larger reductions earned over time.

Driver training discounts apply when the teen completes a state-approved driver education course. Michigan offers a Segment 1 and Segment 2 graduated licensing curriculum — completing both can reduce premiums by 10–15% with most carriers. If your teen already had the accident before completing Segment 2, finishing the course now and submitting proof can still unlock the discount mid-policy.

The distant student discount applies when your teen attends college more than 100 miles from home without a vehicle. If your teen is heading to college and leaving the car at home, notify your carrier immediately — this discount can reduce the teen's portion of the premium by 30–60% while they're away.

How Does the Vehicle Your Teen Drives Affect the Premium After an Accident?

Assign your teen to the oldest, least expensive vehicle in your household with the highest safety rating you own. The vehicle's age, value, and theft risk directly determine collision and comprehensive premiums — a 2015 Honda Civic will cost 40–60% less to insure for a teen driver than a 2022 Dodge Charger, even if both are driven the same number of miles annually.

If the vehicle your teen will drive is paid off, consider dropping collision coverage and keeping only liability and comprehensive. Michigan's unlimited PIP covers medical expenses regardless of fault, so the primary risk you're insuring with collision is vehicle damage. A $4,000 vehicle with a $1,000 deductible and $1,800/year collision premium reaches a point where you're paying nearly half the car's value every two years just for that coverage.

Vehicles with high safety ratings (IIHS Top Safety Pick or Top Safety Pick+) qualify for safety feature discounts with most carriers — automatic emergency braking, lane departure warning, and blind spot monitoring can each reduce premiums by 3–10%. If you're purchasing a vehicle specifically for your teen, prioritize these features alongside low repair costs and theft rates.

What Coverage Do You Actually Need for a Teen Driver With One Accident in Michigan?

Michigan requires unlimited personal injury protection (PIP), $50,000 per person and $100,000 per accident in bodily injury liability, and $10,000 in property damage liability. Parents can opt out of unlimited PIP only if they have qualified health insurance that covers auto injuries, reducing PIP to $250,000 or $500,000 — this can cut premiums by 20–35% but shifts medical cost risk to your health plan.

For a teen driver with one accident, keep your bodily injury liability at least at $250,000/$500,000. Teen drivers are statistically more likely to cause accidents, and Michigan's no-fault system does not prevent third parties from suing for non-economic damages (pain and suffering) when injuries exceed the state's tort threshold. A single serious injury claim can exceed $100,000 quickly, and the judgment follows you and your teen personally if your liability limits are insufficient.

Collision and comprehensive coverage are optional, but if your teen drives a vehicle worth more than $5,000 or the vehicle is financed, keep both. Dropping collision on a $15,000 vehicle to save $1,200/year makes sense only if you can afford to replace the vehicle out of pocket after the next accident — and a teen with one accident already has demonstrated higher risk.

When Should You Shop for New Coverage After Adding a Teen With an Accident?

Shop immediately after adding your teen but before the accident, and again 30–45 days before each annual renewal for the next three years. Rates vary by 40–80% between carriers for the same teen driver and accident profile, and your current carrier is not required to offer you their most competitive rate at renewal — they typically don't.

If the accident happened after you already added your teen to your policy, shop within 30 days of the accident being filed. Some carriers increase premiums immediately upon receiving the claim; others wait until renewal. Switching carriers before your current insurer applies the surcharge at renewal can lock in a lower rate if the new carrier hasn't yet received the accident report through CLUE (Comprehensive Loss Underwriting Exchange).

Re-shop every year for the first three years after the accident. Accident surcharges decrease annually with most carriers, but your existing carrier may not reduce your premium proportionally — they apply the original surcharge percentage to an inflated base rate. A carrier that was not competitive when you first added your teen may become the lowest option 18 or 24 months later as the accident ages off and your teen's driving record improves.