You're looking at a $2,000+ premium increase to add your teen to your policy — and wondering if you can save by dropping collision and comprehensive. Here's the honest math on what you're actually trading.

The Decision Most Parents Face After Seeing the Quote

Most generic insurance advice tells you to buy full coverage for a teen driver because they're high-risk. But that advice ignores the actual decision you're making: whether paying an extra $800 to $1,500 per year for collision and comprehensive coverage makes financial sense when your teen is driving a 2012 Honda Civic worth $6,000. The honest answer depends on three things: what the car is worth, whether it's financed, and whether you can afford to replace it out of pocket if your teen totals it.

According to the Insurance Information Institute, collision and comprehensive coverage typically add 40–60% to a liability-only premium for a teen driver. If liability-only costs $1,800 annually, full coverage might cost $2,700 to $2,900. That extra $900 to $1,100 buys you coverage for damage to your teen's vehicle — but only after you pay the deductible, which is typically $500 to $1,000. If the car is worth $5,000 and you're paying $1,000 extra per year for collision coverage with a $1,000 deductible, you're effectively insuring $4,000 of value at a 25% annual cost. That's not always a bad deal for a teen driver with elevated crash risk, but it's not automatically the right choice either.

The framework that matters: if the vehicle is worth less than three times your annual collision and comprehensive premium, and you could replace it out of pocket, liability-only becomes financially defensible. If the car is financed, you don't have a choice — lenders require full coverage. If it's paid off and worth under $5,000, you're making a calculated risk decision, not an irresponsible one.

What You're Actually Buying With Each Coverage Type

Liability coverage is legally required in nearly every state and covers damage your teen causes to other people and their property. This is non-negotiable. State minimum liability limits are typically $25,000/$50,000/$25,000 (per person injured/per accident injured/property damage), but most insurance professionals recommend at least $100,000/$300,000/$100,000 for a household with assets to protect. If your teen causes a serious accident, liability coverage protects your family from a lawsuit that could reach your savings, home equity, or future wages. This is the coverage you never skimp on, regardless of what your teen is driving.

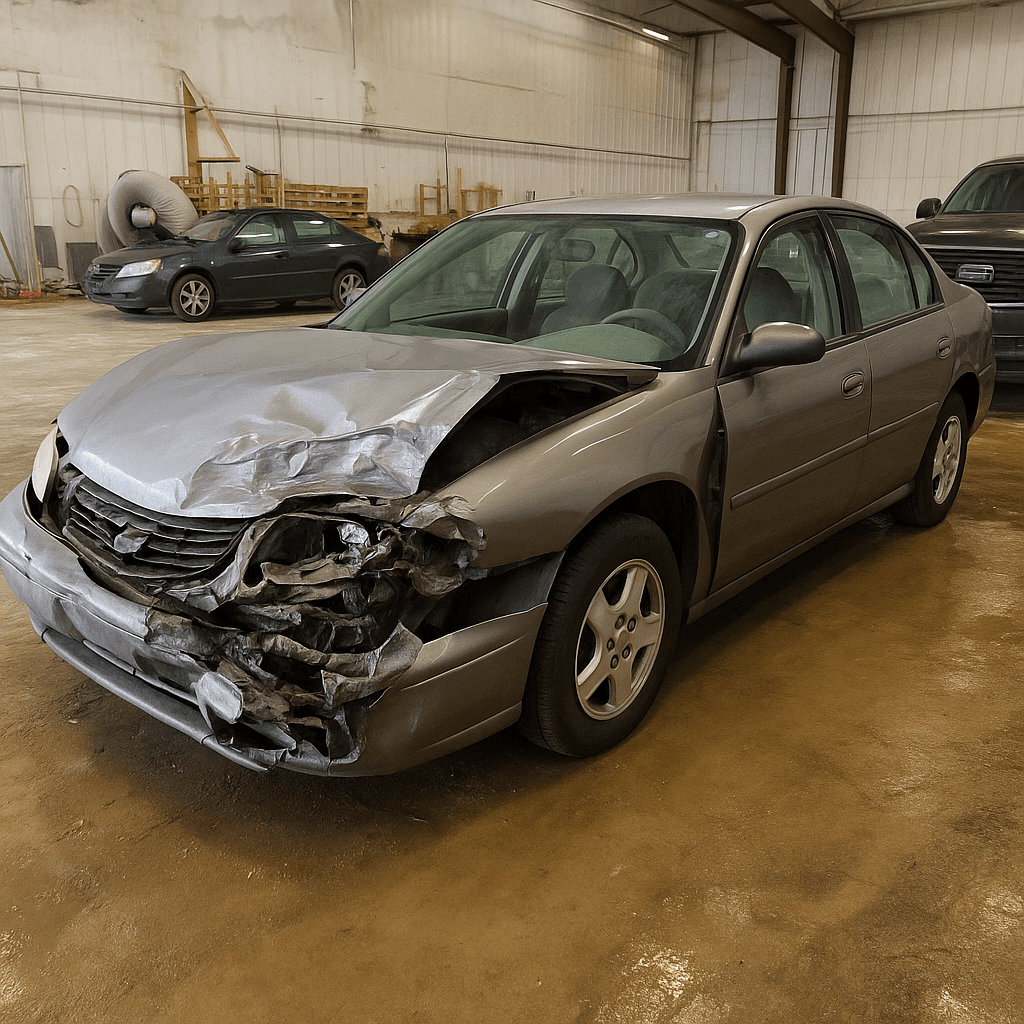

Collision coverage pays to repair or replace your teen's vehicle after an accident, regardless of who was at fault, minus your deductible. If your teen backs into a mailbox, slides off an icy road, or gets hit by another driver who doesn't have insurance, collision covers your car. The Insurance Institute for Highway Safety reports that drivers aged 16-19 have crash rates nearly four times higher than drivers aged 20 and older, which is why collision coverage is expensive for teens — and also why it can be worth the cost if the vehicle has significant value.

Comprehensive coverage pays for damage to your teen's vehicle from non-collision events: theft, vandalism, hail, hitting a deer, or a tree falling on the car. Comprehensive is typically cheaper than collision — often $200 to $400 annually for a teen driver — because it covers risks that aren't correlated with driver age and inexperience. Many parents who drop collision coverage keep comprehensive, especially in areas with high rates of vehicle theft or severe weather.

The Vehicle Value Calculation That Actually Matters

Here's the specific math: look up your teen's vehicle value using Kelley Blue Book or NADA Guides. Subtract your deductible — typically $500 or $1,000. That's the maximum amount your collision coverage will ever pay out. Now compare that to your annual collision premium. If you're paying $900 per year to insure $4,500 of net value (a $5,500 car minus a $1,000 deductible), you're paying 20% of the insured value annually. After five years, you've paid more in premiums than the car was worth.

This calculation changes if your teen is driving a newer or higher-value vehicle. A 2020 model worth $18,000 with a $1,000 deductible gives you $17,000 of insured value. If collision coverage costs $1,200 annually, that's 7% of insured value — a much more reasonable ratio, especially given teen crash rates. The guideline that works for most families: if the vehicle is worth more than $10,000, or if you couldn't comfortably replace it with savings, keep full coverage. If it's worth under $5,000 and paid off, liability-only becomes a legitimate option.

One critical exception: if your teen shares a vehicle with you or drives multiple household vehicles, your decision affects your own coverage. Dropping collision on a car you also drive to save money on your teen's premium is usually a false economy. The better approach is to assign your teen to the lowest-value vehicle in your household and adjust coverage on that vehicle specifically.

When Liability-Only Actually Makes Sense

Liability-only works best when four conditions align: the vehicle is fully paid off, it's worth less than $5,000, you have savings to replace it if necessary, and your teen is driving it exclusively (not sharing a newer vehicle with you). In this scenario, you're self-insuring the vehicle — accepting the risk that you'll pay out of pocket for repairs or replacement if your teen is at fault in an accident. Given that collision coverage might cost $800 to $1,200 annually with a $1,000 deductible, you're effectively betting that your teen won't total the car within the first few years.

That's not a reckless bet if you've prepared for it. Some parents set aside the money they save on collision premiums into a dedicated vehicle replacement fund. If you're saving $1,000 per year and your teen drives for two years without a major accident, you've got $2,000 available to help with a replacement vehicle — which might be more than the depreciated value of the original car anyway. This approach works especially well if your teen is driving a high-mileage vehicle that's reliable but has minimal resale value.

The scenario where liability-only doesn't make sense: your teen is driving a vehicle worth $8,000 or more, or you can't afford to replace the vehicle if it's totaled. In that case, the premium for collision coverage is functioning as intended — it's transferring a financial risk you can't comfortably absorb to an insurance company. The cost feels high because the risk is high, but that's exactly when insurance provides the most value.

The Coverage Options Between Liability-Only and Full Coverage

You don't have to choose between bare-minimum liability and comprehensive-plus-collision. Several middle-ground options reduce cost while maintaining partial physical damage protection. Liability plus comprehensive is the most common compromise: you keep coverage for theft, vandalism, weather, and animal strikes (which aren't related to your teen's driving behavior) but drop collision coverage (which is expensive specifically because of teen crash risk). Comprehensive typically costs $200 to $500 annually for a teen driver — far less than collision — and protects against risks you can't control.

Another option: increase your deductible to lower your premium while keeping full coverage. Moving from a $500 deductible to a $1,000 or $1,500 deductible can reduce your collision premium by 15–30%, according to the National Association of Insurance Commissioners. If you have savings to cover a higher deductible, this lets you keep the protection of full coverage at a meaningfully lower cost. Just make sure you actually have the deductible amount available — a $1,500 deductible saves you nothing if you can't pay it when you need to file a claim.

Some carriers also offer usage-based or low-mileage discounts that reduce premiums if your teen drives fewer than 7,500 or 10,000 miles annually. If your teen only drives to school, work, and weekend activities — and you're tracking mileage through a telematics app — you might reduce your full coverage premium by 10–25%, making it more affordable to keep collision and comprehensive in place.

What Happens If Your Teen Has an At-Fault Accident

If your teen is at fault in an accident and you have liability-only coverage, your insurer pays for the other driver's vehicle and medical expenses up to your liability limits — but you pay out of pocket for all damage to your teen's vehicle. If the car is totaled, you're replacing it entirely with your own money. If it needs $3,000 in repairs, you're paying $3,000. This is the risk you're accepting when you choose liability-only, and it's why this decision should be based on your ability to absorb that cost, not just on monthly budget pressure.

If you have collision coverage and your teen causes an accident, you file a claim with your own insurer, pay your deductible, and the insurer covers the remaining repair or replacement cost. Your premium will almost certainly increase after an at-fault claim — typically by 20–50% for the next three to five years, according to insurance industry data. That rate increase happens whether you have liability-only or full coverage, because it's based on your teen's liability risk to others, not on whether you filed a physical damage claim for your own vehicle.

One important clarification: collision coverage also protects you if your teen is hit by an uninsured or underinsured driver. If another driver runs a red light and totals your teen's car but has no insurance, your collision coverage pays for your vehicle after the deductible. Without collision coverage, you'd need to pursue the at-fault driver directly in small claims court — a process that rarely recovers full value. This uninsured-motorist protection is one of the overlooked benefits of keeping collision coverage even on a modest-value vehicle.

How to Decide for Your Specific Situation

Start with the vehicle value and financing status. If the car is financed or leased, you're required to carry full coverage — this isn't a decision you get to make. If it's paid off, look up the current value and compare it to your annual collision and comprehensive premium quote. If the vehicle is worth less than three years of physical damage premiums, and you have savings to replace it, liability-only becomes financially reasonable.

Next, assess your family's financial cushion. Could you write a $5,000 check tomorrow to replace your teen's vehicle without derailing other financial goals? If yes, dropping collision is a calculated risk. If no, keep collision coverage — the premium is expensive because it's protecting you from a scenario you can't afford. The worst outcome is dropping coverage to save $80 per month, then facing a $6,000 replacement cost you have to put on a credit card.

Finally, consider your teen's specific risk factors. A 16-year-old with a new license in their first year of driving has materially higher crash risk than an 18-year-old who's been driving for two years without incidents. If your teen has completed driver training, maintains a good student discount, and has been driving for at least a year, the actuarial risk is lower — though still elevated compared to adult drivers. Some parents start with full coverage for the first year, then re-evaluate after their teen has demonstrated consistently safe driving. That approach balances protection during the highest-risk period with cost management as your teen gains experience.