You just added your 16-year-old to your Florida policy and the premium jumped $2,400 annually — but they're driving a 2012 sedan you own outright. Here's what coverage you actually need versus what you're paying for.

Why Florida Carriers Quote Full Coverage on Every Vehicle by Default

When you add your teen to your Florida auto policy, carriers generate quotes with collision and comprehensive on every listed vehicle regardless of age or value. A 2012 Honda Civic worth $4,200 gets the same coverage template as your 2022 SUV. The carrier isn't required to explain that you're paying $600-$900 annually to insure a vehicle you could replace out-of-pocket for less than two years of premiums.

Florida requires liability only: $10,000 bodily injury per person, $20,000 per accident, and $10,000 property damage. No state law mandates collision or comprehensive on any vehicle. If you own the car outright with no lienholder requiring coverage, you control the decision entirely.

The business reason carriers default to full coverage is straightforward. Collision and comprehensive premiums fund a significant portion of underwriting profit, especially on teen drivers who statistically file more claims. Removing those coverages from a paid-off older vehicle costs the carrier revenue but doesn't increase their liability exposure. They won't suggest it.

Actual Replacement Cost Math for Vehicles 10+ Years Old

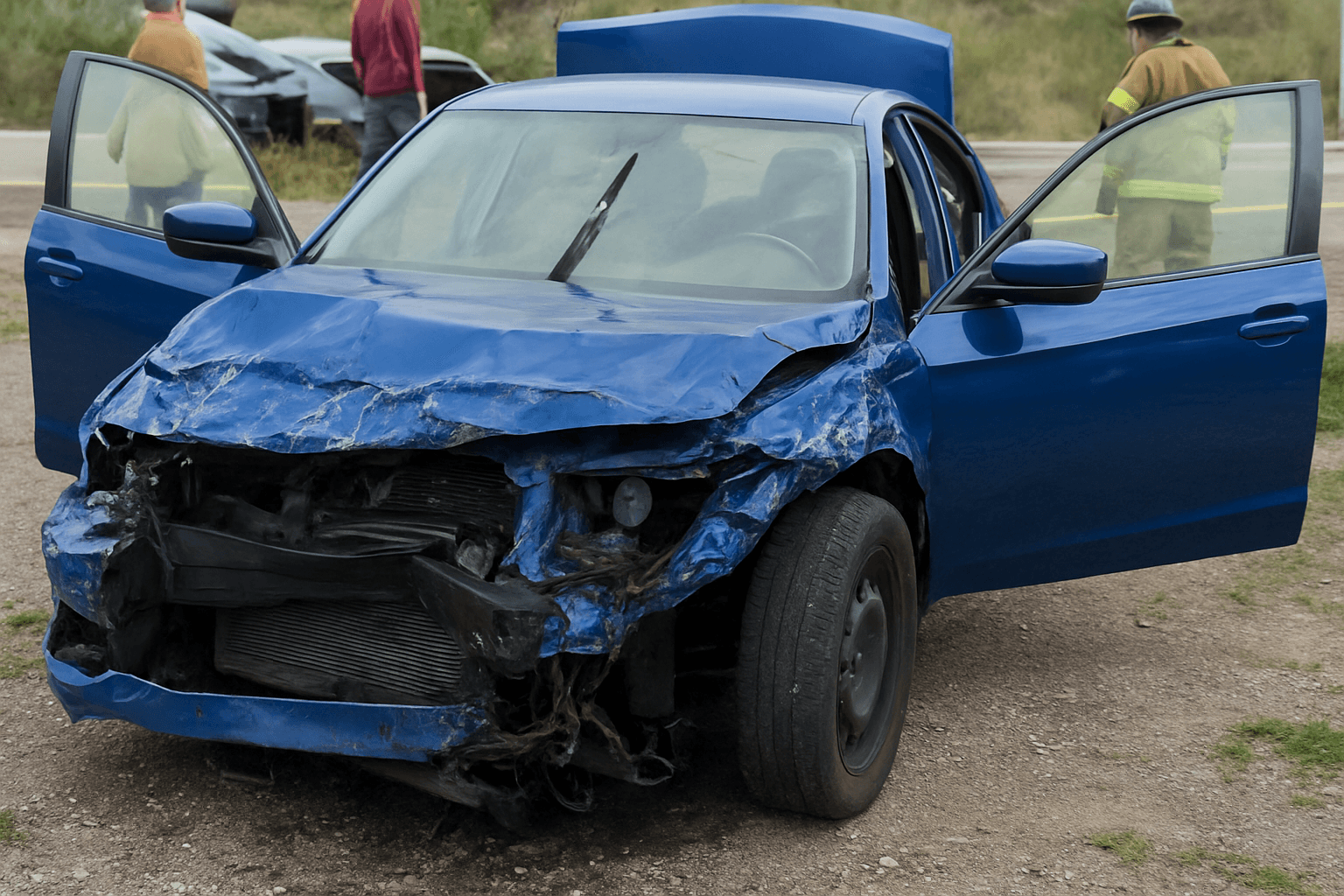

A 2013 model in average condition typically has a market value between $3,500 and $6,500 depending on make, mileage, and maintenance records. Collision coverage on that vehicle with a teen driver listed costs approximately $450-$700 annually in Florida. Comprehensive adds another $180-$250. Combined annual cost: $630-$950.

If your teen totals the vehicle in year one, the carrier pays actual cash value minus your deductible. Assume a $500 collision deductible and a $4,800 payout. Net insurance benefit: $4,300. You paid $650 in premium for $4,300 in coverage — a reasonable transaction if the loss occurs early in the policy period.

But if the vehicle survives two years, you've paid $1,300 in collision and comprehensive premiums to protect a depreciating asset now worth $3,800. By year three, cumulative premiums exceed replacement cost. You're paying the carrier to insure something you could replace cheaper by saving the premium dollars in a separate account.

See what adding a teen driver actually costs in your state

Compare quotes from carriers that offer good student discounts — most parents find savings they didn't know were available.

Get Your Free Quote✓ Good Student Discounts✓ No Obligation✓ Licensed Carriers✓ All 50 States

The Liability-Only Strategy for Paid-Off Teen Vehicles

Dropping collision and comprehensive on your teen's older vehicle and carrying liability only reduces the teen surcharge by 40-50% in most Florida cases. A $2,800 annual increase becomes $1,400-$1,680. You're still paying the liability surcharge because a teen driver increases third-party risk regardless of what they drive, but you're no longer funding first-party physical damage coverage on a low-value asset.

The retained risk is straightforward: if your teen causes an accident, liability covers the other party's vehicle and injuries up to your policy limits, but your teen's car is a total loss you replace out-of-pocket. If another driver hits your teen and is at fault, that driver's property damage liability covers your vehicle regardless of what coverage you carry. The exposure is an at-fault accident where your teen's vehicle is damaged and you pay to replace it.

This strategy makes actuarial sense when the vehicle's market value is below $6,000 and you have liquidity to replace it without financing. It does not make sense if losing the vehicle creates a financial hardship, if your teen commutes long distances daily, or if the vehicle is financed with a lienholder requiring comprehensive and collision.

Florida Graduated Licensing and How It Affects Coverage Timing

Florida issues learner's permits at age 15. Teens must hold the permit for 12 months and complete 50 hours of supervised driving, including 10 hours at night, before applying for an intermediate license at 16. The intermediate license restricts driving between 11 p.m. and 6 a.m. for the first three months, then between 1 a.m. and 5 a.m. until age 17. Passenger restrictions limit non-family passengers under 21 to one for the first six months, then three until age 18.

You must add your teen to your policy the day they receive their learner's permit if they will drive any household vehicle, even under supervision. Florida law does not require separate coverage for permit holders if the supervising driver's policy covers the vehicle, but most carriers require formal listing to ensure premium surcharges apply from the permit stage. Failing to list a permit holder and having them involved in an accident can trigger a coverage denial.

The intermediate license restrictions reduce risk exposure during the highest-risk months, but carriers do not offer measurable premium discounts for GDL compliance. The 11 p.m. curfew for the first three months theoretically reduces nighttime driving risk, but underwriting models price the full annual teen surcharge regardless of GDL phase.

Good Student and Telematics Discounts That Actually Apply in Florida

Florida does not mandate the good student discount, but most carriers writing in the state offer it voluntarily. Qualifying typically requires a 3.0 GPA or better, verified by report card or transcript submission every six months or annually. The discount reduces the teen surcharge by 8-15% depending on carrier — not 8-15% off the total premium, but 8-15% off the teen's incremental cost.

If adding your teen increases your premium by $2,400 annually and the good student discount is 12%, the discount saves $288 per year. You must resubmit proof at each renewal or the discount expires mid-policy without notification from most carriers. Parents who qualified their teen at policy inception but didn't submit updated documentation 12 months later lose the discount silently.

Telematics programs like Drivewise, Snapshot, and SmartRide monitor braking, acceleration, speed, and mileage through a smartphone app or plug-in device. Safe driving behavior during the monitoring period — typically 90 days — can reduce the teen surcharge by an additional 10-20%. These programs are particularly effective for teens driving older vehicles on liability-only coverage because the discount applies to the liability premium, which you're still carrying at full cost.

When Keeping Collision Makes Sense Despite the Vehicle Age

Collision coverage remains justified on older vehicles in three scenarios. First, if your teen's vehicle is their only transportation to school or work and you lack immediate liquidity to replace it after an at-fault accident, the premium cost is cheaper than the disruption cost of losing mobility. Second, if your teen is a new driver with less than six months of unsupervised experience and you assess their at-fault accident probability as high, paying $650 annually for collision is rational insurance if their odds of a claim in the first year are above 15%.

Third, if you carry a high deductible to lower premium and the vehicle's value exceeds $8,000, the coverage remains cost-effective. A $1,000 deductible on a 2014 model worth $8,500 means collision covers $7,500 of at-fault loss. Annual premium with the high deductible might run $380-$450, creating a better cost-benefit ratio than liability-only exposure on a vehicle approaching $10,000 in value.

Financed vehicles remove the decision entirely. If your teen drives a vehicle with an active loan or lease, the lienholder requires comprehensive and collision with a maximum deductible specified in the financing contract, typically $500 or $1,000. You cannot drop coverage until the loan is satisfied and the title is clear.

Uninsured Motorist Coverage and Why It Matters More for Teen Drivers

Florida does not require uninsured motorist coverage, and it's one of the highest uninsured driver states in the country — approximately 20-26% of Florida drivers carry no liability insurance. When an uninsured driver hits your teen and causes injury or vehicle damage, your options without UM coverage are limited to suing the at-fault driver personally, which is rarely productive if they lack insurance due to inability to pay.

Uninsured motorist bodily injury coverage pays your teen's medical bills, lost wages, and pain and suffering claims when an uninsured driver is at fault. Uninsured motorist property damage covers your teen's vehicle damage in the same scenario, subject to a deductible and policy limits. UMPD is particularly relevant if you're dropping collision — an at-fault uninsured driver is not a collision claim, so collision coverage wouldn't respond anyway, but UMPD does.

UM coverage costs approximately $80-$150 annually for a teen driver depending on limits selected. Adding UMPD costs another $40-$70. For a teen driving an older vehicle on liability-only coverage, adding UM bodily injury and UMPD closes the gap left by dropping collision and comprehensive at a fraction of the cost, protecting against the specific risk of an at-fault uninsured driver.