Your teen just got licensed and the family's old Accord is their car now. Do you really need collision and comprehensive on a vehicle worth $4,000, or is liability enough when the premium increase already doubled your bill?

When Full Coverage on an Old Car Costs More Than the Car

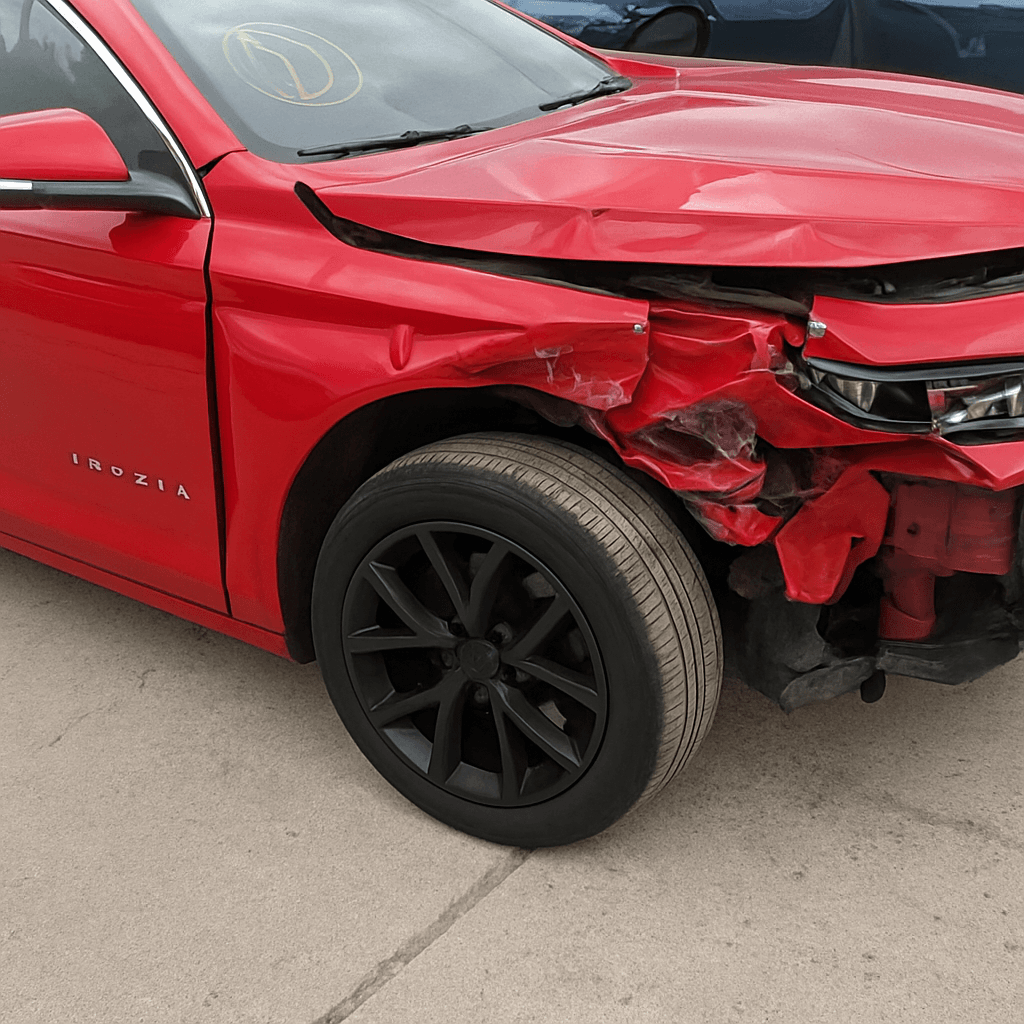

A 2012 Honda Accord in average condition trades for $3,500–$5,500 in New York. Collision and comprehensive coverage on that vehicle with a teen driver typically adds $80–$140/mo to the policy — $960–$1,680 annually. Your deductible is $500 or $1,000. If your teen backs into a pole and causes $2,800 in damage, you pay the deductible and the carrier pays the rest, but your rate increases at renewal.

After two years of premiums, you've paid more than the car's replacement value. If the vehicle is totaled, the carrier pays actual cash value minus your deductible — probably $3,000–$4,500 after depreciation. You've spent $2,000 in collision premiums to insure a $4,000 asset. That math reverses when the vehicle is paid off and worth less than three years of collision premiums.

The coverage floor for a teen driving a paid-off older vehicle in New York is state minimum liability (25/50/10), uninsured motorist coverage, and a separate savings account to replace the car if it's totaled. Collision and comprehensive become optional financial decisions, not requirements.

What New York Requires and What Your Lender Requires Are Different

New York requires $25,000 bodily injury per person, $50,000 per accident, $10,000 property damage, and uninsured motorist coverage at the same limits. Personal injury protection (PIP) at $50,000 is also mandatory. None of those coverages insure your teen's car. They cover injuries and damage your teen causes to others, plus your family's medical bills regardless of fault.

If you still have a loan on the vehicle, your lender requires collision and comprehensive until the loan is paid. The lender is listed as loss payee — if the car is totaled, the check goes to them first. Once the title is clear, that requirement disappears. You can drop collision and comp the day the loan is satisfied if the math supports it.

Most parents keep full coverage out of habit or fear, not because the policy requires it. Check your loan balance and your vehicle's trade-in value. If the car is worth $4,500 and you owe $800, you're one payment away from dropping $1,200/year in coverage costs.

See what adding a teen driver actually costs in your state

Compare quotes from carriers that offer good student discounts — most parents find savings they didn't know were available.

Get Your Free Quote✓ Good Student Discounts✓ No Obligation✓ Licensed Carriers✓ All 50 States

The Liability Limit Decision When a Teen Is on the Policy

State minimum liability (25/50/10) is the legal floor but not the recommended floor when a teen driver is on the policy. A teen driver backing out of a parking space and hitting a pedestrian can generate a $100,000 injury claim in seconds. Your liability coverage pays up to the policy limit; you pay everything above it from personal assets.

Increasing liability limits from 25/50/10 to 100/300/100 typically adds $15–$35/mo to the total policy cost — far less than the $80–$140/mo collision and comprehensive cost on an older vehicle. If you're dropping collision to manage costs, reallocate that budget to higher liability limits. The financial exposure from an at-fault injury accident is always larger than the replacement cost of a 2012 sedan.

Uninsured motorist coverage in New York must match your liability limits unless you reject it in writing. Keep it. Roughly 5–8% of New York drivers are uninsured, and if an uninsured driver totals your teen's car or injures your teen, this coverage responds. It's the most undervalued line on the policy.

How Dropping Collision Affects a Claim After an At-Fault Accident

If your teen is at fault and collision coverage is not on the policy, the other driver's property damage is covered by your liability coverage but your teen's car is not covered at all. If your teen totals the family Accord by running a red light, you pay to replace it out of pocket. The rate increase happens either way — filing a collision claim or being found at fault both trigger surcharges.

If another driver is at fault and has insurance, their property damage liability covers your teen's vehicle. You file a claim against their policy, not yours. Your coverage doesn't apply and your rate doesn't increase. If the at-fault driver is uninsured, your uninsured motorist property damage coverage responds if you carry it — many New York policies include it, but it's not mandatory and some parents waive it to reduce premiums.

The risk you're accepting by dropping collision is paying replacement cost after an at-fault accident. The rate increase happens regardless of whether collision is on the policy. The question is whether paying $1,200/year to insure a $4,000 car makes sense when the surcharge for an at-fault accident will cost you more than the collision premium savings over three years anyway.

How Vehicle Choice Affects the Add-to-Policy Premium Increase

Adding a 17-year-old driver to a New York policy increases the annual premium by $2,500–$4,500 depending on the vehicle, coverage, and location. That range is not random. A teen listed as the primary driver of a 2023 Subaru WRX will generate a $5,000–$7,000 increase. A teen listed as an occasional driver of a 2012 Honda Accord will generate a $2,200–$3,200 increase.

Carriers rate teen drivers by the vehicle they drive most often. If you have three vehicles on the policy — a 2020 Civic, a 2015 Accord, and a 2012 CR-V — and you assign the teen to the CR-V, the surcharge applies to that vehicle's rate. Assign them to the newest vehicle and the surcharge applies to the higher base rate. The total increase can differ by $1,500–$2,500 annually.

This is why many parents buy an older paid-off vehicle for the teen rather than adding them as the primary driver of a newer financed car. The collision and comprehensive premiums on the older car are lower, the teen surcharge applies to a lower base rate, and if the teen wrecks it, you're not upside-down on a loan.

Good Student and Telematics Discounts Stack on Top of Vehicle Savings

The good student discount in New York is not state-mandated — it's carrier-discretionary. Most carriers offer 8–15% off the teen portion of the premium for maintaining a 3.0 GPA or better. You must submit a report card or transcript every six months or annually depending on the carrier. Some carriers ask for it; others don't. If you don't submit documentation at renewal, the discount drops off mid-policy without notification.

Telematics programs from Progressive (Snapshot), State Farm (Drive Safe & Save), Allstate (Drivewise), and Geico (DriveEasy) monitor braking, acceleration, speed, and time of day. Safe driving behavior can reduce the teen surcharge by 10–30% after the monitoring period. These programs are opt-in and require app installation or a plug-in device. They work particularly well for teens driving older vehicles in rural or suburban areas where speeds are lower and hard braking events are less frequent.

Stacking both discounts — good student and telematics — can reduce the teen add cost by 18–40%. That reduction applies whether or not you carry collision. The discount comes off the liability and uninsured motorist surcharge, not just physical damage coverage.

When Keeping the Teen on Your Policy Stops Making Sense

If your teen is heading to college more than 100 miles away and not taking the car, most carriers offer a distant student discount of 10–35% on the teen portion of the premium. The vehicle stays on your policy but the teen is listed as an away-at-school driver with no regular access. You'll need to provide proof of enrollment and school address annually.

If the teen is taking the car to school or moving out and keeping the vehicle, the cost calculus changes. A separate policy for a young driver with no prior insurance history will cost $3,600–$6,500 annually in New York depending on location and coverage. That's often higher than the add-to-parent-policy cost, but it removes the teen's rate impact from your policy and allows you to drop collision on the older vehicle without affecting your own coverage.

The breakeven point is typically when the teen turns 21–23, has two years of clean driving history, and qualifies for their own policy at a rate lower than the surcharge they add to yours. Until then, keeping them on your policy and managing discounts is almost always cheaper.